On March 5, news broke that Japanese automobile giant Nissan Motor had been unilaterally slashing payments to over 30 subcontractors in its business alliance, or keiretsu. Reports suggest the reductions amounted to as much as ¥3 billion JPY (approximately $20 million USD) over the past several years. Nissan has been making these cuts for several decades.

Toshiba, once one of Japan's leading consumer electronics manufacturers, has also been in trouble. On December 20, 2023, it was delisted from the Tokyo and Nagoya Stock Exchanges. Toshiba's downfall was triggered by its 2006 acquisition of Westinghouse, a nuclear power company. The $5.4 billion investment in Westinghouse proved fatal.

As its performance stagnated, Toshiba's decline accelerated in 2015 with the discovery of its window dressing. Following its takeover by a Japan Industrial Partners-led consortium, the conglomerate was finally delisted.

This news signifies a major shift in keiretsu, the unique corporate structure that supported Japan's postwar industry.

Understanding Keiretsu

A keiretsu is a conglomeration of companies across various sectors, including banks and trading companies. Mitsubishi, Mitsui, Sumitomo, Fuyo, DKB Group, and Sanwa are the six major keiretsu. Nissan Motor is a member of the Fuyo Keiretsu, and Toshiba is a member of the Mitsui Keiretsu.

Keiretsu's origins can be traced back to the zaibatsu, a group of diverse businesses owned exclusively by a single family. Before World War II, the zaibatsu constituted the basis of Japan's economy. Mitsubishi, Mitsui, and Sumitomo were the three major zaibatsu, each wholly owned by the Iwasaki, Mitsui, and Sumitomo families, respectively.

After World War II, the General Headquarters for the Occupation, known as GHQ, dismantled the zaibatsu system. In its place emerged new corporate groups: keiretsu. The six major keiretsu groups (Mitsubishi, Mitsui, Sumitomo, Fuyo, DKB Group, and Sanwa) led Japan's postwar economy.

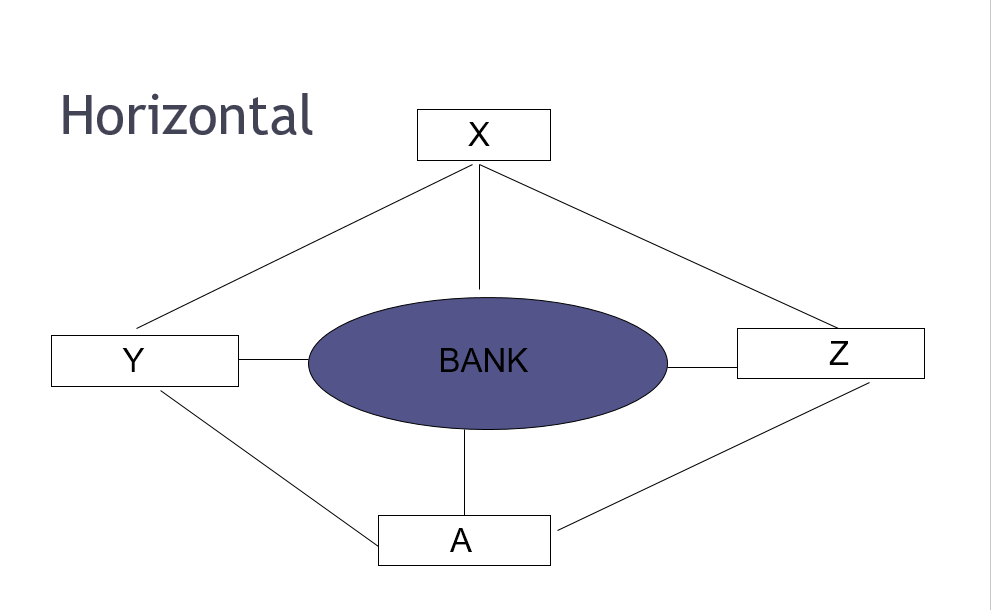

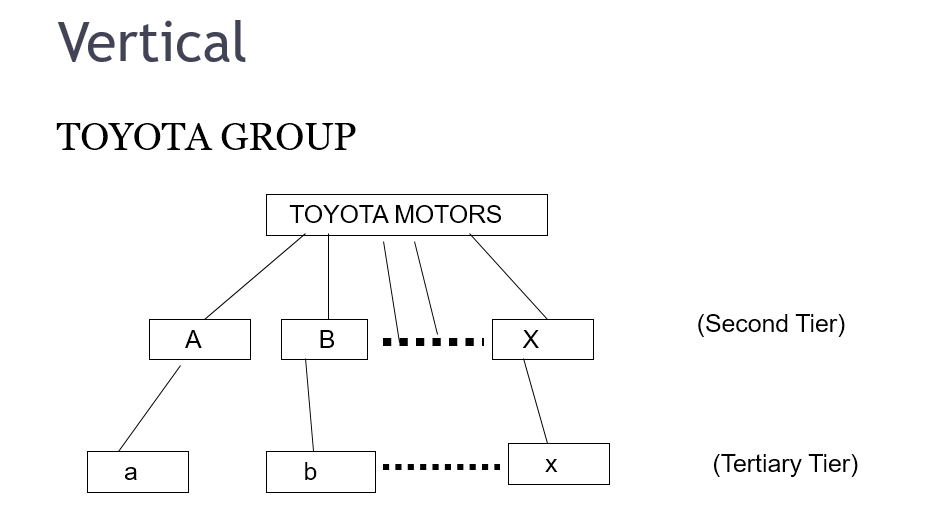

While a single-family controlled the zaibatsu, keiretsu resulted from strong intra-company ties. Keiretsu fall into two patterns according to differences in relations among the companies within the group: horizontal and vertical keiretsu.

Cross-shareholdings

Cross-shareholdings among the same affiliated groups are a feature of horizontal keiretsu. By holding one another's shares, keiretsu member companies stabilized their respective share prices. Refusing to relinquish their holdings in member companies has also discouraged takeover attempts by outside parties.

Keiretsu comprise a wide range of businesses. For example, one keiretsu company might procure raw materials from overseas through an affiliated trading company. This company would then supply its products to other member companies, creating a mutually beneficial business relationship.

Vertical keiretsu link suppliers, manufacturers, and distributors in a given industry. Automobile manufacturer Toyota is a typical example. Toyota's steering wheel manufacturer supplies exact quantities based on the number of cars to be produced that day. This low-cost production system, which also keeps inventory costs at a minimum, is called the just-in-time method. During the 1980s, it was a hot topic across US business schools.

After the Bubble Economy

Japanese banks were among the top seven banks in the 1991 global rankings. However, those that had functioned as command centers for their respective keiretsu soon began to lose ground. Regional bank bankruptcies and the sale of Long-Term Credit Bank of Japan in the late 1990s symbolized this. The creation of megabanks through the merger of several banks also heralded the end of this golden age.

Furthermore, poor corporate performance and stock price slumps have led some keiretsu companies to release their shares in allied keiretsu companies. Cross-shareholdings among keiretsu firms have also declined.

In 1999, French automobile manufacturer Renault helped save Nissan Motors from the brink of bankruptcy. That year, the company dispatched Carlos Ghosn to Nissan as CEO. Some credit Ghosn with reviving Nissan by implementing thorough cost-cutting measures.

Under his management, however, Nissan began to procure expensive parts from companies outside the Nissan group. Reducing costs in the face of sluggish sales growth contributed to higher profits.

However, it has emerged that Nissan had illegally slashed payments to subcontractors to meet its cost-cutting and production expansion targets. Ghosn's cost-cutting brand of management seemed to have rescued Nissan. Now signs indicate that his measures weakened the keiretsu's solidarity and undermined Nissan's ability to sustain and strengthen its growth.

Towards a New System

In the past, when a keiretsu member company faced trouble or difficult circumstances, the keiretsu's core bank would help. These banks would increase loans and dispatch personnel to help the company get back on its feet. Other member companies would provide full support, including capital contributions.

However, as Toshiba faced delisting, it did not receive support from its keiretsu members at levels of the past. Cross-shareholdings that stabilized the share price have reached their limits. More companies are now increasingly selling off cross-shares to lock in profits.

Japan's real wages fell 0.6% in January over the same month in 2023, the 22nd consecutive month of decline. Since real wages have been slow to rise, the government has asked companies to raise wages. Some larger companies have subsequently announced wage hikes.

The question is whether employees of subcontractors within the same keiretsu will also receive wage increases. Sacrificing subcontractors to increase wages for major firms would be unfair. It was fine when the economy was doing well, and wages were rising accordingly, as was the case before the bubble era.

With the economy still in deflation, however, raising wages is not only an issue for individual companies. It concerns every company within the entire keiretsu to which it belongs. Ultimately, it will be a problem for all workers in Japan.

Whether horizontal or vertical, it is becoming increasingly difficult for keiretsu to function optimally in their current conception. Member firms must cooperate, pool their wisdom, and endeavor to develop a system that responds to the ever-changing economic environment.

RELATED:

- EDITORIAL | Nissan Case a Warning to Firms with Unfair Trade Practices

- Bank of Japan Announces First Rate Hike in 17 Years

- EDITORIAL | Delisting Toshiba is Necessary, Must Lead to Drastic Reforms

Author: Yoshifumi Fukuzawa

With a lengthy background in international banking, Yoshifumi Fukuzawa is a business consultant and lecturer at Waseda University.